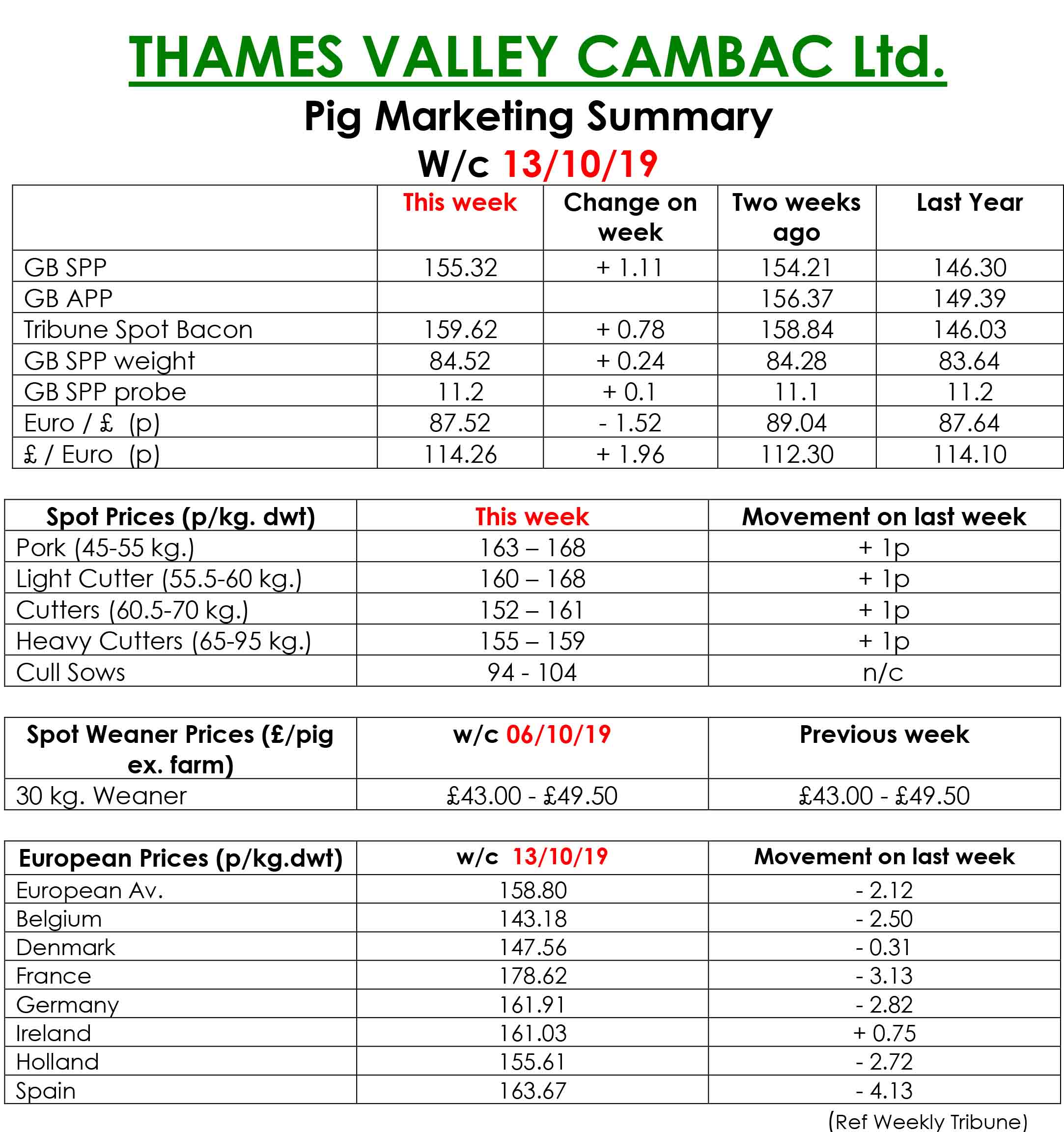

This week’s Pig Marketing Summary, from Thames Valley Cambac, reported that the market was similar with supply slightly higher and demand in a steady vein. Some processors were still dogged by poor retail demand, but a good undercurrent of export trade ensured all pigs were placed.

The markets ability to kill more is limited at the moment by the lack of cold store space – Christmas storage and possible Brexit buffer stocks taking precedence. Prices moved up on the whole, helped by a good lift in the SPP – up 1.11p, the highest one week rise in 17 weeks, and weekly contract contributions up 1p to 2p.

The fresh meat market was a touch quieter, but prices still appreciated with quotes generally 1p better. In spite of adverse currency movements, the cull sow market stood on pricewise and volumes were similar.

In Europe, Ireland and Denmark added 4 and 2.5 euro cents respectively, while Spain eased down 1.5 euro cents. Price quotes in sterling were tempered further by a weaker Euro that ended the week down 1.52p at 87.52p – its lowest level in five months.

The Weaner Marketing Summary, for week commencing October 6, reported that supply continued to outweigh demand, with many fatteners reluctant to bid for any supplies outside contract arrangements. A lack of good quality fattening accommodation does not help the situation.

The prices announced by the AHDB a 30kg store pig quoted at £50.99 and the weighted average for a 7kg weaner rise by 35p to £40.10p.