Demand has been fluctuating across the pork market, reflecting changes in Chinese export prospects and the recent closure of most European foodservice outlets, according to the latest numbers from AHDB.

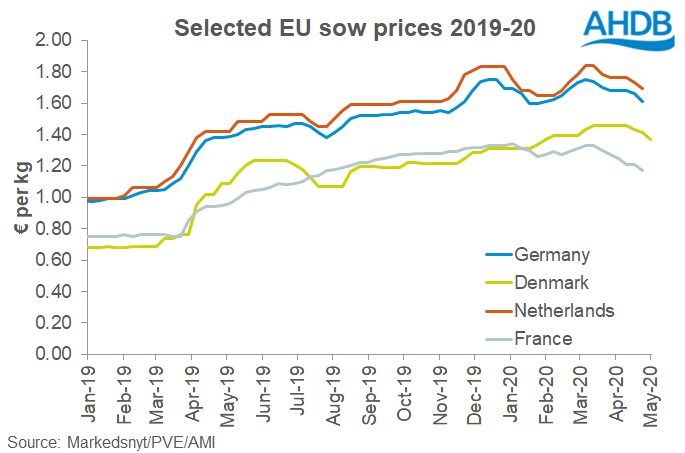

Sow prices in the EU have shown some volatility across the main markets since February, following the pattern in the finished pig market. There was some uplift in February, but fortunes have since turned and quotes for the latest week are now lower than the start of the year, although still significantly higher than the same period in 2019.

Reports suggest demand has been insufficient for supply and cold stores have been filling, and prices have therefore been falling.

AHDB analyst Bethan Wilkins explained that due to close trade links to the German sow market, GB cull sow prices tend to follow the German M1 sow price. Ms Wilkins said: “Reports already indicate the recent drop in the German market has fed through to prices here, with booking slots also reportedly lower as export demand suffers.

“Moving cold storage volumes continues to be challenged by both the lack of European foodservice demand and difficulties with container availability constraining exports. As a net pork exporter, Germany is particularly sensitive to limitations on its export market. Although, the upcoming grilling season might provide some support to German consumption, especially if Germans are unable to take their usual foreign holidays. Nonetheless, there is still no real clarity around when the current challenges may ease, and so the British sow market faces a period of uncertainty.