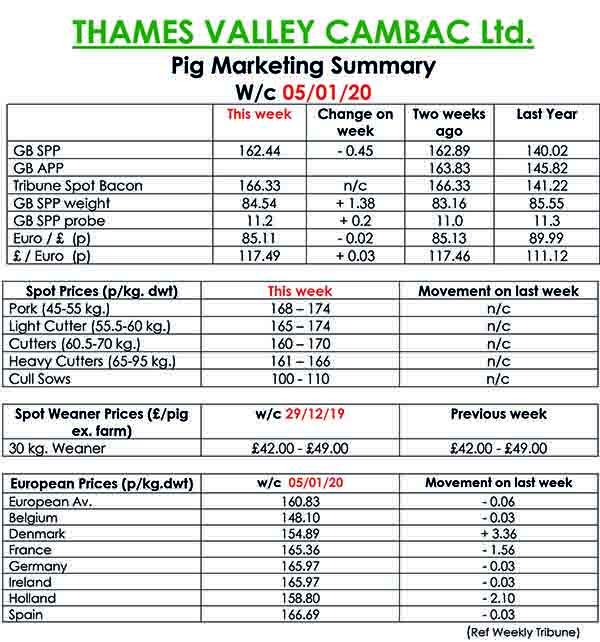

This week’s Slaughter Pig Marketing Summary, from Thames Valley Cambac, reported that the first full week of the New Year is traditional for the supply chain to be replenished, and so it proved with this week’s trading.

Demand was brisk from the majority of majors, although there were exceptions. Contract contributions stood on, but some prices slipped due the late announced SPP dropping 0.45p to162.44. This fall, albeit surprising, on further investigation shows that the sample is half the size of normal, with bigger and fatter pigs within it.

The subsequent SPP should be back to normal. The fresh meat market saw steady demand, again refilling the supply lines, and prices remained similar. The cull sow market started up again and prices were similar to pre-Christmas.

In Europe, Denmark’s quote improved four euro cents, but there were falls in Holland and France. Prices quotes in sterling were compromised further by a slightly weaker euro that ended the week down 0.02p at 85.11p.

The Weaner Marketing Summary, for week commencing December 29, reported that demand remained steady, and movements were limited to regular trades only.

The prices announced by the AHDB saw no quote given for a 30kg store pig, and the weighted average for a 7kg weaner rise by £1.02 to £42.50p.