Primary pigmeat sales remained strong as overall pigmeat volumes declines, according to the latest UK retail sales data from Worldpanel by Numerator UK, summarised by AHDB.

In the 12 weeks to May 17, total pig meat purchase volumes declined by 3.4%, 7,339 tonnes, year-on-year, with spend down by 3.1% and average prices up by 0.3%.

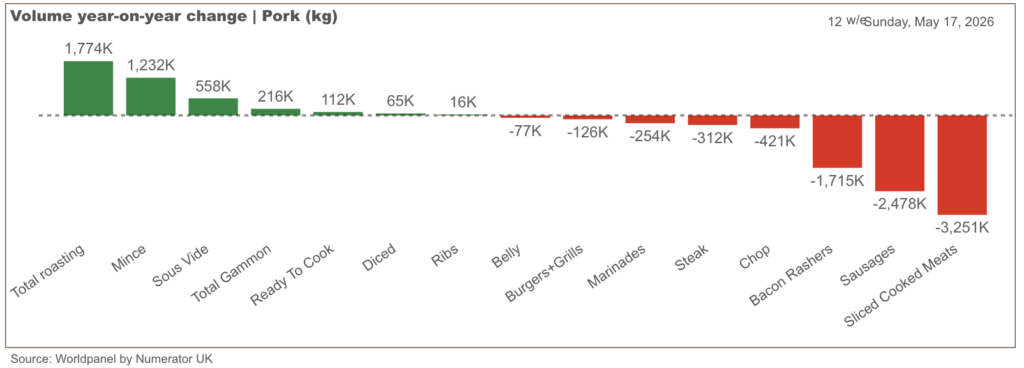

Within the overall volume decline, primary pigmeat, where the UK is strongest, performed well, with purchase volumes increasing by 6.8% and spend up 5.5% year-on-year.

Volume growth was driven by mince, up by 30.1%, as consumers switch from beef mince to the cheaper pork option, while roasting joints volumes were 16.5% higher due to higher numbers of shoppers and volumes per shopping trip. Within that category, leg roasting was up by 30.9%, shoulder up by 11.7%, but loin was down by 18.3%. Chop volumes were down 14.8%, while diced pork was up 31.1%.

In contrast, processed pig meat purchase volumes fell by 5.9%, driving the overall category decline. Bacon volumes were down 5.7%, (-1,715 tonnes), sausages were down 5.9%, (-2,478t) and sliced cooked meats 9.1% (-3,251t). According to AHDB, this was potentially driven by concerns around ultra processed foods driving lower purchase frequency.

Added-value pig meat products also continued to grow, with purchase volumes increasing by 4.7% year-on-year. Spend rose alongside this, with shoppers buying larger volumes per trip. This was led by sous vide products, with volumes up 13.2%, while ready to cook was up 9.1%, although spend was down due to lower prices. Marinade volumes were down 7.6%.

Beef and lamb

Over the same period, total beef retail volumes were down by 4%, although spend was up by 7.5%, driven by a 12% higher hike in prices.

It is well documented that soaring beef prices and falling volumes over the past year or so have boosted pork volumes. The latest figures show that, although volumes are still declining, the rate of decline has slowed compared to previous periods, suggesting ‘some slight easing in pressure on shoppers’, according to AHDB.

Total lamb retail spend increased by 7.8% year-on-year over the 12-week period, driven by higher prices and a small 0.9% increase in volumes.

Porkwatch latest

Meanwhile, the May AHDB Porkwatch survey continues to show steady support among the big UK retailers for British pork.

Across the 10 retailers surveyed, 87% of pork on display was British, slightly down on March and in line with a year ago. Aldi, Co-op, Lidl, M&S, Morrisons and Sainsbury’s were all on 100%, Waitrose 98% (100% own label), Tesco 84% and Asda 58%, down from the March figure. Iceland stocked just 3% British.

The overall figure for bacon, 56%, was also slightly down on March and in line with May 2025. Co-op and M&S displayed 100% British, with Waitrose on 93%. At the other end of the scale, Aldi, Lidl and Asda were on 21%, 23% and 25%, respectively, with Iceland on 11%.

A total of 63% of ham was British, slightly up on March and a year ago, with M&S, 98%, Coop, 95% and Waitrose, 86%, leading the way. Morrisons, 42%, Lidl, 41%, Asda, 39% and Iceland, 14%, stocked the lowest proportion of British.

The overall proportion of British sausage, 79%, was slightly down on March, but up on a year ago. M&S, 100%, Aldi, 99%, Waitrose, 96% and Lidl, 93%, stocked the highest proportion of British sausage. Apart from Iceland, 50%, no other retailer dropped below 70%.