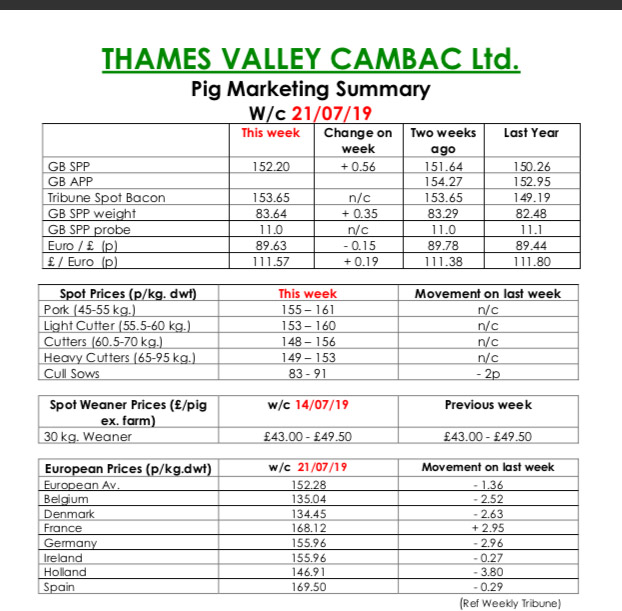

This week’s Slaughter Pig Marketing Summary, from Thames Valley Cambac, reported that trade continued to be subdued with lacklustre retail demand being blamed by most of the processors. A major breakdown on Friday caused a not insignificant rescheduling of the early week, but all pigs were eventually placed. Supplies generally improved, helped by better growth rates in recent weeks.

All contract price contributions stood on, giving a stable feel to the market. The fresh meat market continued in a similar vein, – quiet, steady trade. The cull sow market continued to slide, losing another 2p on the back of weaker continental prices. In Europe, France bucked the trend adding 3.5 euro cents, whilst Germany and it’s other near neighbours fell another 3 to 4 euro cents in response to Germany’s loss of the Philippine export market reported last week.

It is unfortunate that the price differential between our market and near Europe is closing due to the latter falling, instead of our prices rising. Price quotes in sterling were further eroded by a weaker Euro that ended the week down 0.15p at 89.63p.

The Weaner Marketing Summary, for week commencing July 14, reported that supplies continued to improve with 7kgs weaners especially plentiful. However, there was little interest from the majority of fatteners, who stuck with committed contract supplies, but little else. The prices announced by the AHDB saw the weighted average for a 30kg store pig quoted at £54.15, and the weighted average for a 7kg weaner rise by 21p to £38.04p.