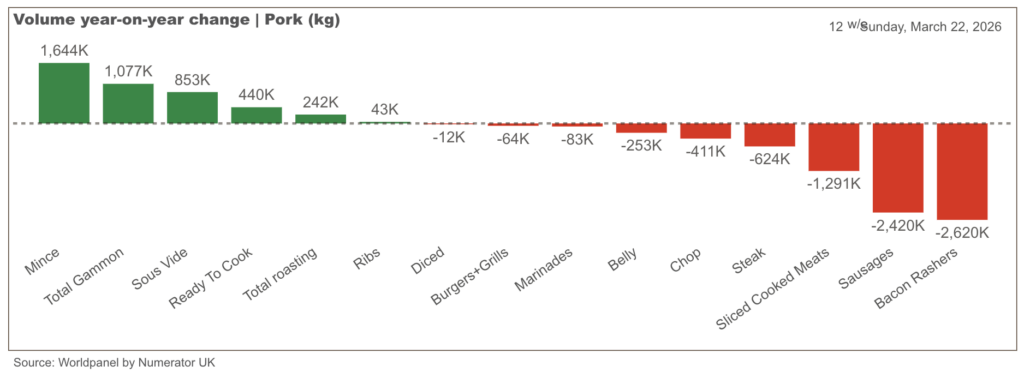

Retail pigmeat volumes were down 2.3% year-on-year over the first quarter of 2026, with value down 0.6% on the back of higher prices, according to data from Worldpanel by Numerator UK, summarised by AHDB.

This represents a return to the downward trend, after a welcome year-on-year volume and value increase in 2025.

However, primary pigmeat volumes, where British product is strongest, were up 1.1% over the 12 weeks ended March 22, with mince again the best performer (+39.3%).

The losses came in the processed pigmeat category, with volumes down 4.3%. Total gammon saw a 8.6% increase in volumes, but bacon was down 11.6% and sausage 4.3%.

Total added value volumes were up 16.8%, driven by sous vide which saw a 22.2% increase, with ready-to-cook up 40.4%.

Porkwatch latest

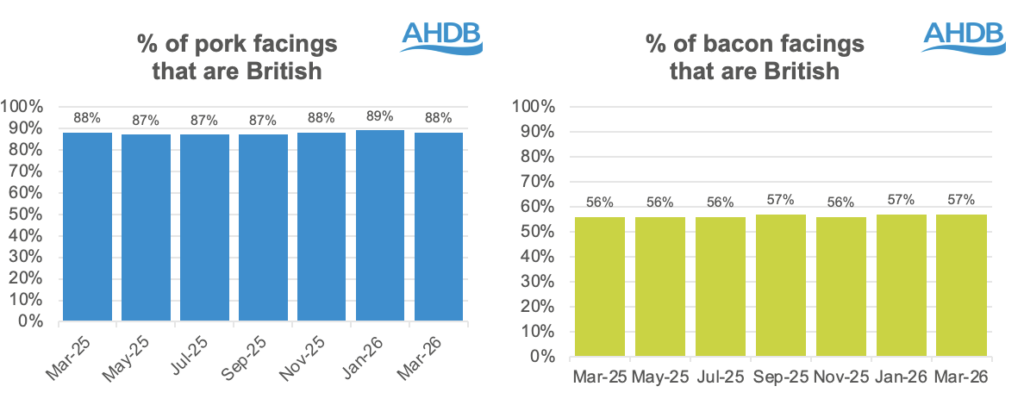

However, the latest Porkwatch survey showed retail support for British pork products remains historically strong. Across all 10 retailers surveyed in March, 88% of pork on display was British, slightly down on the high of 89% in January, but in line with the March 2025 figure.

Aldi, Co-op, Lidl, Morrisons, M&S and Sainsbury’s were all 100% British, with Waitrose on 99% (100% own label), Tesco 84%, Asda 62% and Iceland just 1%.

The March figure for bacon, 57%, was in line with January and slightly up on the same month in 2025. Co-op and M&S were both 100% British, with Waitrose on 93%, but Asda, Aldi, Lidl and Iceland all below 30%.

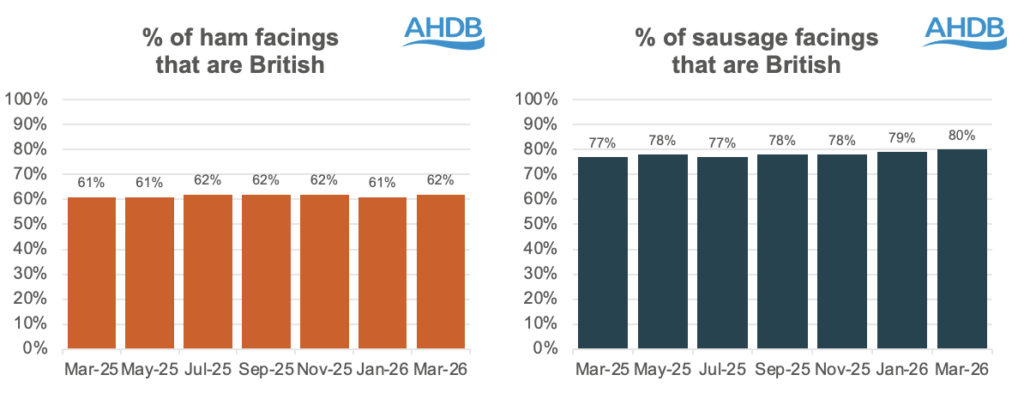

The latest figures for ham and sausage, 62% and 80%, respectively, were both higher than January and March 2025.

M&S (98%), Co-op (94%) and Waitrose (87%) led the way on ham, with M&S (99%), Aldi (98%), Waitrose (96%) and Lidl (93%) displaying the highest proportion of British ham.