UK pigmeat export volumes grew in 2025, driven by increased demand from China as it became embroiled in trade tensions elsewhere, while UK import volumes fell.

Exports

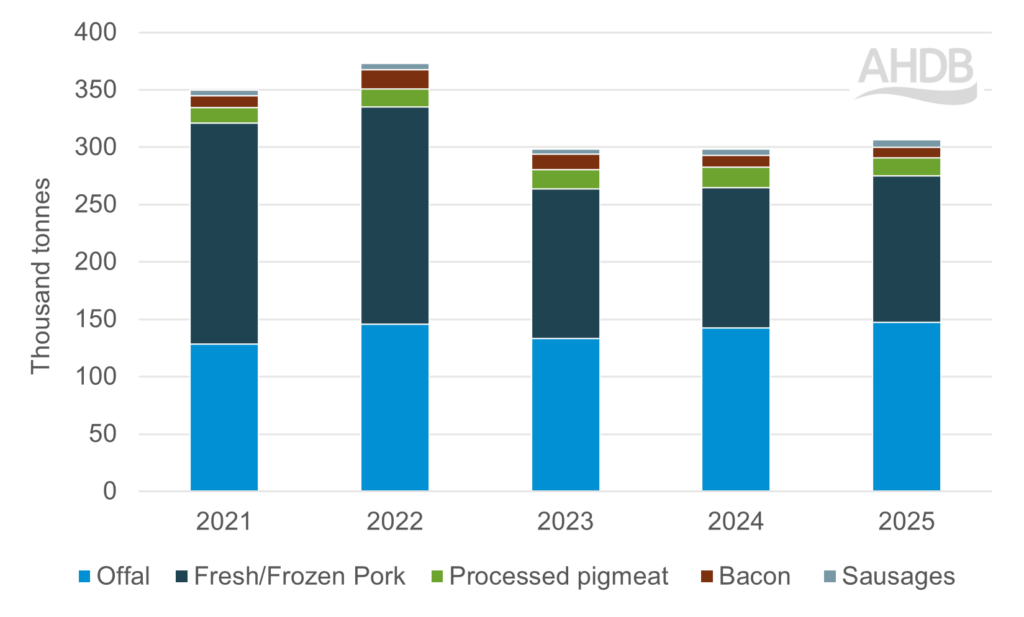

UK pigmeat export volumes grew by 2.6% to 306,200 tonnes in 2025, although the value of the shipments was down by 4.7% to £492 million.

The biggest single category was offal, accounting for 48% of total volumes – exports, at 147,200t, were up 3.1%,

Fresh and frozen pork, representing 42% of exports, saw volumes grow by nearly 5% to 128,000t, while sausage exports recorded the strongest growth, rising 11% to 6,100t.

There were year-on-year volume falls for bacon, down 8% to 9,500tm and processed products, including ham, down 12% to15,600t.

AHDB analyst Adam Chowdry said the overall growth was ‘spurred by a growth in domestic production and rising demand from key trade partners’.

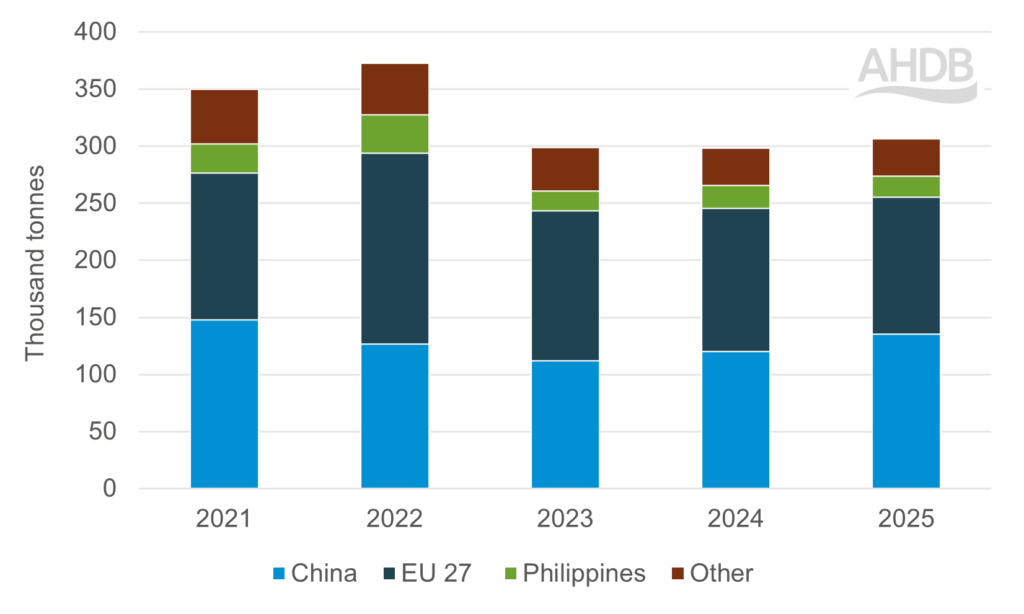

The 2025 export volume gains came in non-EU shipments, which were up 7.8% to 186,700t, while EU pigmeat exports were 4.5% lower at 119,500t.

China was the largest export destination in 2025, overtaking the EU in terms of volume. Shipments to China rose by 13% (15,500t), totalling 135,600t, with offal shipments up 14.7% to 90,000t and fresh and frozen pork shipments 9.9% higher at 45,500t.

The China growth was supported by trade tension between China and other trade partners, Mr Chowdry added.

Non-EU exports outside China declined, driven largely by reductions to the Philippines (-9%). This trade continues to be affected by increasing competition from Brazil, which is putting pressure on suppliers like the UK, the USA and Canada.

Imports

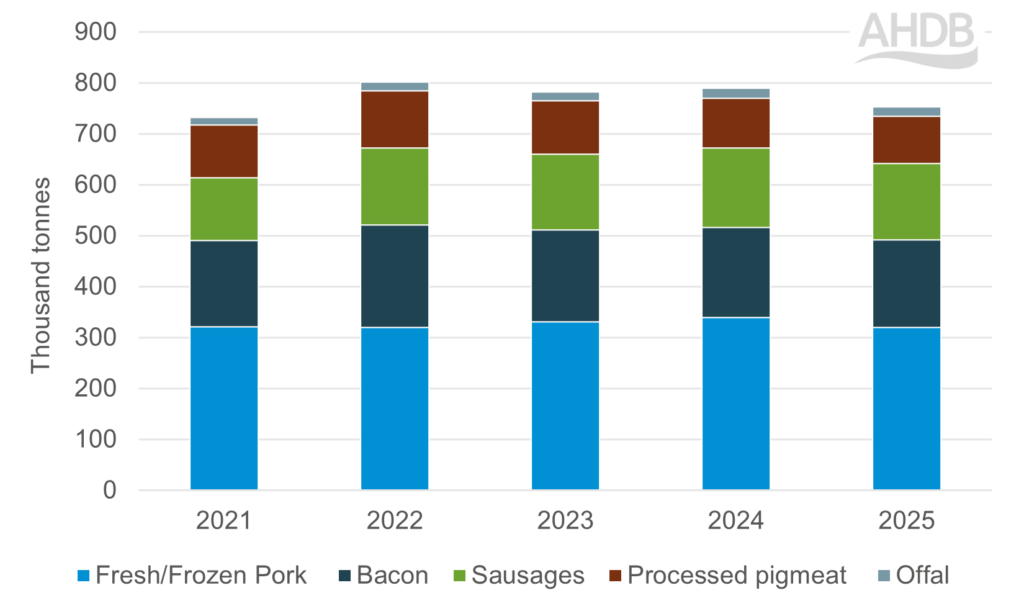

Total UK pigmeat import volumes were down by 4.8% to 752,500t in 2025, with volumes lower in all categories.

Germany recorded the sharpest decline, with shipments falling by 26% (37,000t) year on year to 104,200t, largely due to the import ban imposed early in the year following its foot‑and‑mouth disease outbreak.

Belgium recorded the strongest growth among EU suppliers, increasing shipments by 12% to 56,500t over the year.

The US remained the largest non-EU supplier, although volumes were comparatively small, with US imports down 28% to 1,100t.

Mr Chowdry pointed out that the significant fall in EU prices during the latter part of 2025 did not translate into a material increase in UK import volumes.

Overall, Q4 imports fell by 7% (15,300 tonnes) YoY, underscoring the broader downward trend observed across 2025.

“Monthly trade patterns show fluctuation throughout the year, with a modest uplift in October and November, likely reflecting seasonal demand ahead of Christmas,” he said.

“However, December imports fell by 9% (5,800t) year on year, and both November and December volumes were lower than the previous four years. This suggests that, despite the widening UK–EU price differential, demand for British product remained resilient.”

Data from AHDB’s bi-monthly Porkwatch audit show that British facings remained steady across the period.

While import volumes declined overall, product shares remained broadly similar. Fresh and frozen pork import volumes declined by 6% (19,500t), equalling 43% of total imports. Denmark, Belgium, Spain and Germany remained the principal suppliers.

Bacon imports fell by 3% (5,600t), representing 23% of volumes. Key suppliers were the Netherlands, Denmark and Ireland.

Sausages declined by 3% (4,600t) accounting for 20% of imports, while processed pig meat fell 5% (4,900t), representing 12% of total volumes.

Offal recorded the steepest percentage decline, down 15%, although it only accounted for 2% of the total import share.